Everyone’s dazzled by videos of humanoid robots making coffee or tidying up a factory floor, thinking the final frontier is just a few clever algorithms away. But while you were watching a slick demo, the real war for the future of robotics was being fought in a far less glamorous place: a bill-of-materials spreadsheet.

A sobering new report from McKinsey & Company, “Turning humanoid supply-chain constraints into billion-dollar wins,” cuts through the AI hype with the cold, hard logic of manufacturing. The single biggest hurdle to a future teeming with robotic helpers isn’t their brain; it’s their body, and the brutal economics of building it. The typical cost to assemble one humanoid today ranges from a pricey $30,000 to an eye-watering $150,000. The magic number for mass adoption? Somewhere under $20,000. That’s not a gap; it’s a chasm, and it’s carved out of components.

The $150,000 Problem

So, where does all that money go? The cost breakdown reveals a startling dependency on one specific area. While sensing and perception systems make up 10-20% of the cost, and compute platforms another 10-15%, the lion’s share is devoured by the robot’s muscles.

The breakdown of a typical humanoid’s Bill of Materials (BOM):

- Actuators: 40-60%

- Sensing & Perception: 10-20%

- Compute & Control: 10-15%

- Structure: 5-10%

- Battery: 5-10%

Actuators—the motors and gear systems that create movement in the joints—are not only the most expensive component but also the primary performance differentiator. They are, quite literally, what makes a robot work. And herein lies the fundamental problem: the supplier ecosystem for the high-performance, compact, and powerful actuators that humanoids require is dangerously underdeveloped.

This creates a classic chicken-and-egg dilemma. Suppliers won’t pour millions into building dedicated, high-volume production lines for specialized actuators because humanoid order volumes are still measured in the dozens, not the thousands. But volumes stay pathetically low precisely because the high cost of these low-volume components keeps the final price of a robot astronomically high.

China’s Electric Vehicle Head Start

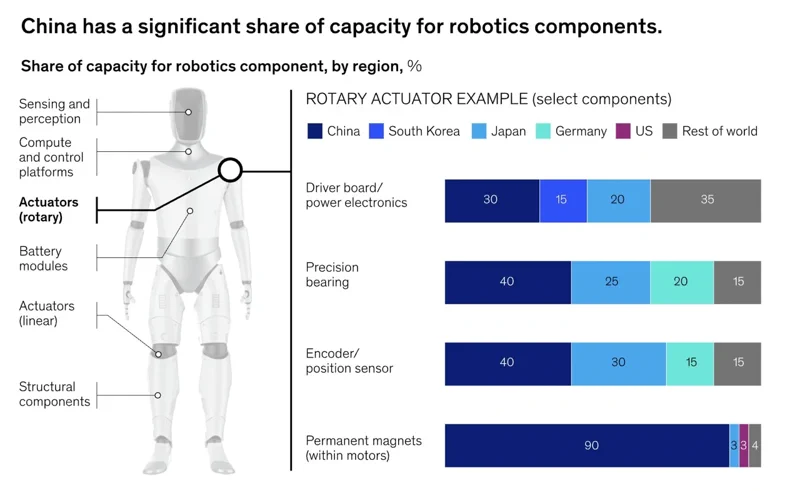

This scaling impasse has one glaring exception: China. The McKinsey report highlights a massive structural advantage that has little to do with robotics and everything to do with another industry: electric vehicles. China’s colossal, mature, and deeply integrated EV supply chain has a direct and powerful overlap with the needs of humanoid robots.

Key components like high-torque motors, power electronics, precision bearings, and, most critically, permanent magnets are already produced there at a scale the rest of the world can’t match. The report notes that China produces 90% of the permanent magnets and 40% of the precision bearings and encoders used in humanoids. One analysis cited by McKinsey found that building a Tesla Optimus Gen 2 without Chinese suppliers would cause its BOM to triple from roughly $46,000 to $131,000. This isn’t a minor cost difference; it’s a game-changing competitive moat.

This advantage is already on display. Chinese manufacturers like Unitree are listing their G1 humanoid for as low as $16,000, a price point Western firms can currently only dream of.

The West’s Response: Build or Partner?

Faced with this supply chain reality, Western robotics companies are scrambling for a solution. Two main strategies have emerged: vertically integrate and build everything yourself, or partner with an established manufacturing giant.

Tesla is the poster child for the first approach. Leveraging its hard-won experience in scaling EV production, the company is designing its own custom actuators, motors, and control electronics for the Optimus robot. It’s a slow, capital-intensive strategy, but if successful, it could provide Tesla with an untouchable cost and performance advantage, completely sidestepping the supplier bottleneck.

On the other side is Figure AI, which has taken the partnership route. In a landmark deal, the company is deploying its robots in BMW’s manufacturing facility in South Carolina. This gives Figure a high-volume, real-world customer to help justify scaling production while offloading some of the manufacturing integration challenges. It’s a faster path to market, but one that relies on the willingness of partners to co-invest and solve the scaling problem together.

The uncomfortable truth is that neither path is easy. While the world remains fixated on the next viral video of a robot performing a human task, the real race is happening far from the cameras. It’s a battle being waged by supply chain managers, procurement teams, and manufacturing engineers. The company that solves the sub-$20,000 bill of materials problem first won’t just win the market; they’ll create it.