Let’s address the elephant in the cleanroom. While venture capitalists scramble to throw cash at the latest bipedal marvel, a rather inconvenient truth is hiding in plain sight: despite the billions poured in, the actual amount of useful work these advanced robots perform is, to put it politely, a rounding error.

In a recent, surgically precise dispatch, Dyna Co-Founder Yang York took a scalpel to the industry hype, and the picture he paints is far from pretty. Forget those glossy demo videos of robots performing parkour or delicately poaching an egg. The real story lies in the data, and it reveals a profound disconnect. Between 2022 and 2025, the robotics sector swallowed over $18 billion in funding. Yet, as we move into early 2026, the real-world impact remains vanishingly small.

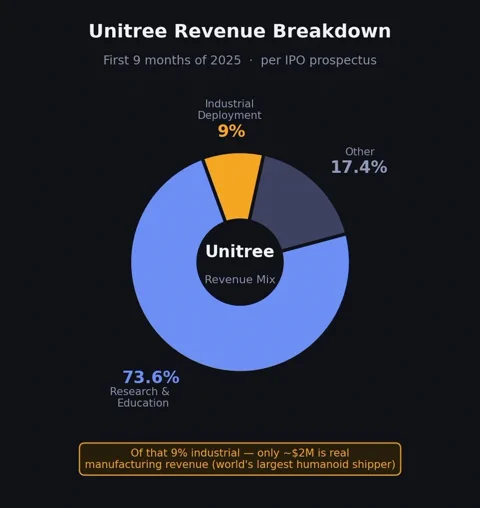

York points to the poster children of the hardware boom to illustrate his point. During a January 2026 earnings call, Tesla’s Elon Musk admitted that effectively zero Optimus units were actually doing productive work in his gigafactories. Meanwhile, Unitree, arguably the world’s most prolific shipper of humanoids, revealed in its March IPO prospectus that a staggering 73.6% of its revenue came from research and education sales. Actual industrial deployment? A mere 9%, the majority of which was limited to “enterprise reception and tour-guide” duties. The revenue generated from genuine manufacturing tasks was a paltry ~$2 million.

This chasm between sky-high financial expectations and physical reality is what York defines as the bubble. It’s not a question of whether the tech will eventually work; it’s a question of the timeline. As he puts it: “A bubble is the gap between current technical capability and human expectations, multiplied by time.”

Your LLM Analogy is Bad, and You Should Feel Bad

A central pillar of York’s argument is that the robotics industry is high on its own supply—specifically, a set of fundamentally flawed analogies. Investors and founders, intoxicated by the exponential growth of Large Language Models (LLMs), are attempting to apply the same playbook to the world of atoms. It is failing spectacularly.

LLMs scaled at breakneck speed because they are pure software, capable of being distributed instantly to billions via the web. Robots, however, are stubbornly physical. They break. They require maintenance. They must navigate the messy, unpredictable chaos of the physical world.

The more tempting—and equally flawed—analogy is the autonomous vehicle (AV) industry. But even that doesn’t quite fit. A car is a useful tool even without self-driving capabilities; it’s an established product category with a distribution network just waiting for an AI upgrade. A non-intelligent humanoid, York quips, is simply “a 27kg machine with 28 degrees of freedom and no purpose.” It has no built-in user base. There is no installed infrastructure to upgrade. The industry is trying to build the app, the handset, and the entire mobile network all at once.

Consequently, robotics won’t follow an LLM-style takeoff curve. It won’t even follow an AV-style curve. It will have a robotics-shaped curve, and the industry’s refusal to accept this reality is its most expensive mistake to date.

The Three Great Deceptions of Modern Robotics

York identifies three core fallacies propping up the current hype. These are the comforting myths the industry tells itself while cashing another nine-figure cheque.

1. Hardware is Not a Channel

The most expensive misconception is the idea that shipping a physical robot is equivalent to building a distribution channel. The logic is: get the hardware into a customer’s facility, and the rest will follow. This is a fatal error.

A real channel creates recurring value. If a robot performs a demo and then sits in a corner gathering dust because it can’t clear the ROI bar, you don’t have a channel. You have a very expensive paperweight. York argues that a true robotics channel is a full-stack deployment system: site assessment, task definition, data capture, remote debugging, and continuous over-the-air updates.

“The test of a channel is whether the tenth deployment is faster than the first,” York writes. “If it isn’t, you haven’t built a channel. You’ve just built inventory and PR.”

2. Your “Foundation Model” is Mostly Foundation

The second error is a fundamental misunderstanding of how AI models actually achieve competence. The robotics conversation has been dominated by pre-training on massive datasets. But the “secret sauce” of modern LLMs isn’t just pre-training; it’s the tight, iterative loop between pre-training and domain-specific, post-training feedback.

Robotics has barely scratched the surface of this loop. Most teams are force-feeding models more data, praying for emergent capabilities. But without the post-training signal from real-world deployments—from robots actually failing on a factory floor—the models cannot mature. There is no unified metric, like an LLM’s “perplexity,” to optimise against. A model that aces a benchmark in a lab is useless if it can’t handle a shift in lighting in a real-world warehouse.

3. The Flywheel is Made of Boring Stuff

This leads to the most underestimated part of the stack: the deployment infrastructure. This isn’t just about sales; it’s the gritty, unglamorous engineering required to turn a bespoke deployment into a reusable, compounding asset. It’s the tooling for remote diagnostics, data routing, and rock-solid reliability.

Without this “flywheel,” the entire system grinds to a halt. The robot never makes it into real environments. The model never gets the real-world data it needs to improve. The capability curve flattens, regardless of how much compute you throw at it. The bubble, York argues, “lives in the gap between teams that have understood this and teams still chasing benchmark numbers and viral demo videos.”

The Only Way Out is Through

Faced with this reality, the field has split. Some are model-first, betting that a sufficiently powerful “brain” will solve the problem and hardware will eventually become a commodity. Others are hardware-first, believing the perfect body is the key and that open-source software will fill the gaps.

York and Dyna are firmly in the third camp: vertical integration. They didn’t choose it because it’s trendy; they chose it because, after a year of deploying their DYNA-1 model, they found the alternative to be impossible. They learned the hard way that deployment doesn’t magically become easier over time. The feedback loop must close across research, hardware, and deployment simultaneously.

This is the hard graft ahead. It’s not about chasing the next viral clip. It’s about the painstaking process of building a system that makes the tenth deployment faster and more reliable than the first. The first team to truly crack that code won’t just win the market—they’ll define it. Until then, we’re all just spectators at a very expensive science fair.